Must Be 21 To Enter

By entering this site you are agreeing that you are at least 21 Years of Age or older.

I AM 21 OR OLDERA Dispensary's Guide to Payment Processing Security

.svg)

.png)

A busy Saturday at a DC dispensary creates the kind of payment mess most retailers never have to think about. One customer wants to pay in cash at the counter. Another inserts a debit card for a PIN transaction. Meanwhile, a delivery order is waiting in a third-party platform, and staff are trying to confirm whether the payment step, the customer data, and the delivery handoff are all locked down.

That's why payment processing security in cannabis isn't just about stopping hackers. It's about controlling a fragmented system where in-store, curbside, and delivery payments often run through different tools, different workflows, and sometimes different companies. If you own or manage a dispensary, the biggest risk usually isn't one dramatic failure. It's the quiet gap between systems, people, and vendors where nobody is fully sure who owns the risk.

The Unique Payment Challenge for DC Dispensaries

On paper, taking a payment sounds simple. In a DC dispensary, it rarely is.

A normal retail store can lean on standard credit card rails and treat payment security as a mostly settled vendor problem. A cannabis business can't. Due to the federal-level illegality of cannabis, major credit card processors like Visa, Mastercard, and AMEX explicitly prohibit knowingly participating with any marijuana businesses, making it legally impossible for dispensaries to accept standard credit card payments. A patient trying to use a Visa card at a DC dispensary would be denied at the point of sale, which is why merchants need compliant alternatives like PIN debit instead, as explained in Flowhub's dispensary payment processing guide.

That one restriction changes everything downstream. Staff end up handling more cash. Managers have to think harder about debit workflows. Online orders need a compliant prepay option. Delivery adds another layer because the payment page, menu, and checkout logic may sit inside a separate platform.

Why the problem gets harder in omnichannel sales

In-store transactions are one thing. Delivery and curbside create a different risk profile.

When you run a hybrid operation, the payment journey may start on your menu, move through an embedded ordering flow, and finish with a handoff to a driver or curbside runner. If one piece of that chain is managed by a third party, your exposure doesn't disappear. It just gets harder to see. That matters in DC, where local compliance expectations and operating rules shape how dispensaries build patient-facing workflows. A useful background read is this overview of how D.C. regulates medical cannabis dispensaries.

The real security problem in cannabis payments isn't only the transaction. It's the handoff between payment, fulfillment, and compliance.

Alternative payments solve one problem and create another

Cash reduces reliance on prohibited credit card networks, but it raises theft and reconciliation risk. PIN debit creates a more controlled in-store option, but the terminal, network path, and user permissions still need protection. Delivery prepay can reduce cash exposure, but now the dispensary has to trust the online environment where the order is placed.

That's the tradeoff many owners miss. They think, “We found a cannabis-friendly payment method, so the hard part is over.” It isn't. The hard part is knowing where cardholder data, bank data, customer identity checks, order records, and checkout scripts live, and who's responsible for each part when something breaks.

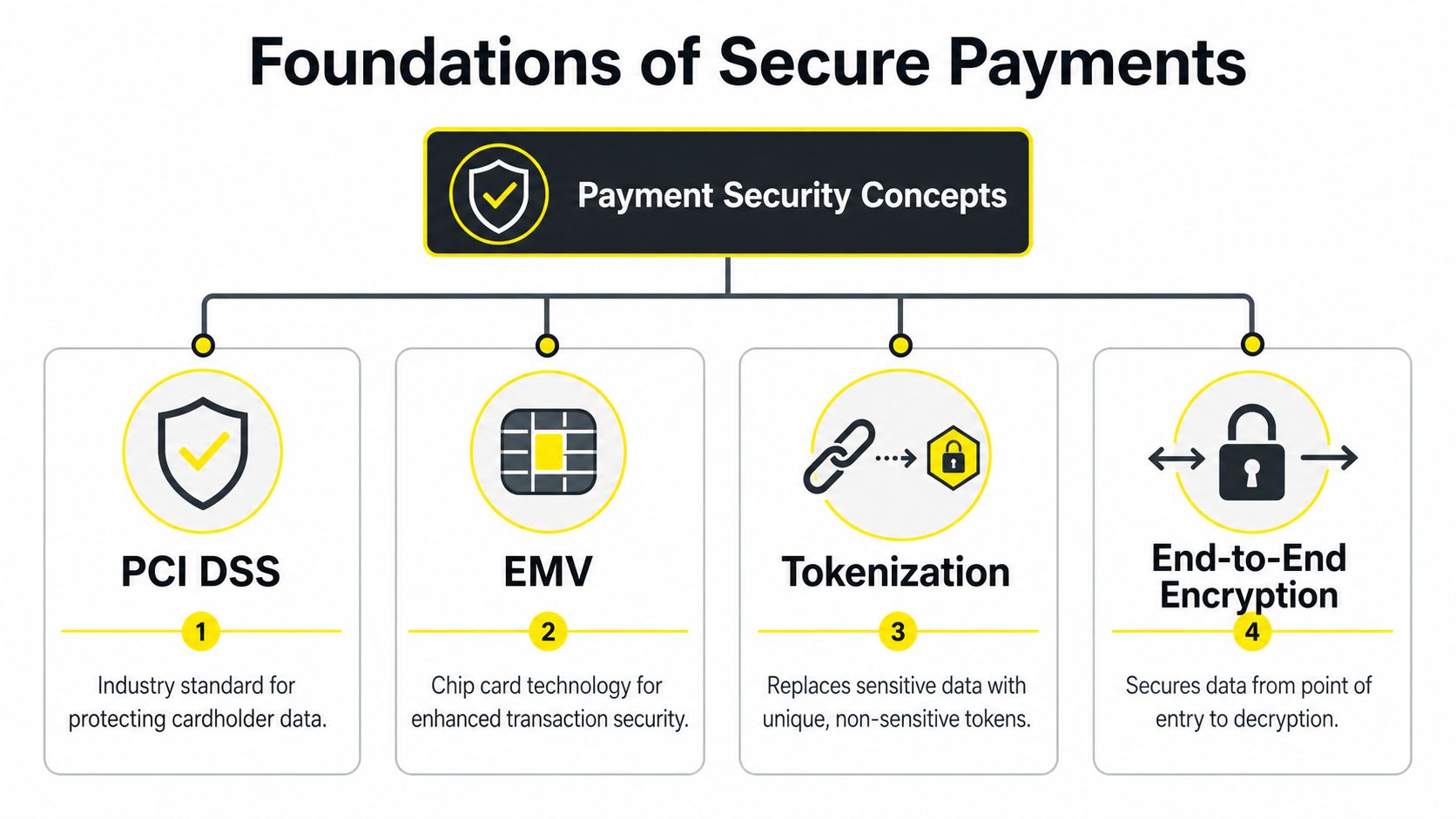

Understanding Core Payment Security Concepts

Most owners hear a string of terms from processors and software vendors and nod along. PCI DSS, EMV, tokenization, and end-to-end encryption sound familiar, but they often blur together. They're not the same thing, and if you mix them up, vendors can hide weak security behind good marketing.

PCI DSS is the building code

Think of PCI DSS as the building code for payment environments. It sets the rules for how payment data should be handled, protected, and monitored. It doesn't guarantee safety by itself, just like a building code doesn't stop every fire. But if a vendor can't clearly explain how their system supports PCI obligations, that's a warning sign.

For a dispensary owner, the practical question is simple. Which systems touch payment data, and which people can affect those systems?

That's where many operators get tripped up. They assume only the payment terminal matters. In reality, any connected device, admin panel, plugin, or online checkout component can affect payment processing security if it can influence how payment data is handled. Similar discipline applies in adjacent compliance workflows such as age verification for cannabis orders, where a weak front-end process can undermine a compliant policy.

EMV, tokenization, and encryption do different jobs

A chip card terminal using EMV helps reduce certain kinds of card fraud during an in-person transaction. It's about making the transaction harder to counterfeit at the point of sale.

Tokenization is different. Use the coat-check analogy. A customer hands over something valuable, and the system gives back a claim ticket that's useless to anyone else. The payment system stores or passes a token instead of the sensitive payment data itself. If someone steals the token, they don't get the underlying account details.

End-to-end encryption protects data while it travels. Think of it as sealing the payment information inside a locked tube from the moment it enters the terminal until it reaches the place authorized to decrypt it. Without that, data can be exposed while it moves between systems.

Practical rule: If a vendor says they use encryption, ask where data is encrypted, where it is decrypted, and who controls the keys.

The network matters as much as the payment app

Many dispensaries still think in terms of “secure software” and ignore the surrounding network. That's a mistake. Payment environments must use micro-segmentation to isolate the Payment DMZ from general business networks, enforce zero-trust networking where every connection is verified regardless of source, and implement FIPS 140-2 Level 3 certified Hardware Security Modules for critical key management to prevent unauthorized decryption of cardholder data, as described in Secure Systems' payment security guidance.

Here's the plain-English version:

- Micro-segmentation: Your payment systems shouldn't sit on the same open neighborhood street as office laptops, printers, cameras, and guest Wi-Fi.

- Zero-trust networking: A device isn't trusted just because it's “inside” your environment. Every connection has to prove it belongs.

- Hardware Security Modules: The keys that decrypt encrypted payment data should be stored in specialized hardware, not casually tucked into application logic.

If your POS, office email, inventory workstation, and delivery management tablet all share broad access, your payment setup is too flat.

Common Payment Threats and How They Appear

A Friday night rush is underway. One budtender is checking IDs, another is fixing a stuck receipt printer, and a delivery order just came in through your online menu. Money is moving through three channels at once. That is exactly when payment threats hide in plain sight.

The easy-to-miss in-store problems

In-store threats are often boring, ordinary, and expensive.

A compromised terminal may still process cards normally. A swapped device, a hidden overlay, or a loose cable can blend into a busy checkout counter. Staff are focused on line speed, ID verification, and customer questions. An attacker counts on that distraction.

Internal abuse usually looks even more routine. A cashier voids a sale after the customer leaves. Two employees share one login because it saves time. A manager-level account edits records no one reviews closely. Those are not rare edge cases. They are control gaps that create clean cover for theft, refund abuse, and missing inventory tied to bad payment records.

A useful test is simple. Walk the store like someone trying to hide a bad transaction. Where could you change a record without a second set of eyes? Where could you touch a payment device without anyone noticing? Those answers usually point to the actual weak spots faster than a policy manual will.

Delivery adds script risk and a vendor accountability problem

Delivery changes the threat model. The obvious concern is the driver carrying product, cash, or a mobile device. The less obvious concern sits on the checkout page before the driver ever leaves.

The risk ownership gap shows up in real life. A dispensary may own the customer relationship and take the financial hit from a dispute, but the online checkout flow may run through a third-party ordering or delivery platform. That platform may load scripts for analytics, chat, fraud tools, menu widgets, or payment functions. If one of those scripts is altered or injected, customer and payment data can be captured during checkout.

The problem is not just the script itself. The problem is unclear ownership. The dispensary assumes the vendor is watching the page. The vendor assumes the merchant approved the integration and accepts the exposure. Meanwhile, no one is actively checking what code is running during payment or who signed off on a change.

For a dispensary using a platform like Sweede, this matters across in-store pickup, curbside, and delivery. One order may start on a branded menu, pass through a hosted cart, and finish on a mobile device in a car. Each handoff creates another place where responsibility can get blurry.

Ask direct questions:

- Which scripts run on the payment page?

- Which company owns each script?

- Who approves changes?

- How are new scripts detected?

- Who investigates if checkout behavior changes overnight?

If a vendor cannot answer those plainly, you do not have a technical problem alone. You have a governance problem.

This matters even more in online buying flows built to feel fast and easy, like the experience described in this guide to the online weed ordering process. Smooth checkout helps sales. Untracked third-party code can stealthily turn that same checkout into a collection point for stolen data.

Friendly fraud is still a payment threat

Some losses come from a real customer using a real account. McKinsey explains that payment fraud programs need to separate different fraud types, including first-party fraud, in its analysis of resilient payments systems.

For a dispensary, that often looks like this. A customer places a delivery order, receives it, then claims it never arrived. Another customer disputes the charge after the product is consumed and frames the problem as an unauthorized transaction instead of buyer's remorse or dissatisfaction. The cardholder is real. The order may be real too. The fraud sits in the story told afterward.

That is why proof matters so much in cannabis delivery. If your records do not clearly show who ordered, who accepted, when the handoff happened, and what device or workflow captured that evidence, the dispute team is left arguing from memory.

A short explainer on attack patterns helps teams spot the difference between system abuse and ordinary service issues.

The practical lesson is simple. Payment threats in a dispensary do not stay in one lane. They show up at the counter, inside staff permissions, in third-party checkout scripts, and in delivery disputes where everyone assumes someone else owns the risk.

Implementing Practical Security Controls

Security controls need to fit real dispensary operations. If a control slows the line to a crawl, staff will work around it. If it depends on perfect behavior every day, it will fail. Good payment processing security uses layered controls that still work on a hectic shift.

Start with the counter and the cash drawer

At the store level, the basics still matter most.

- Lock down terminal access: Each staff member needs an individual login. Shared credentials make investigations useless.

- Inspect devices at open and close: Train shift leads to look for damaged seals, new attachments, loose cables, or terminal swaps.

- Separate payment duties from refund authority: The person taking a payment shouldn't automatically be the person who can void or alter it without review.

- Reconcile daily: Match drawer totals, terminal reports, and order records before people go home.

If you still accept a meaningful amount of cash, treat it like inventory. Cash disappears fastest when no one owns the count at each handoff.

Use the safest payment rail for the right channel

Different channels need different controls.

For online prepay, pickup, and delivery, ACH payments are generally permissible for cannabis sales and are recommended as the safest, most reliable, and most consumer-friendly solution for smooth payments. A concrete example from Goodwin's cannabis payment processing analysis describes a customer ordering Gelato flower for delivery to Alexandria and completing the transaction through ACH bank transfer before the driver arrives, avoiding the risks of carrying cash while staying within federal compliance guidelines.

For in-store purchases, use a compliant debit workflow rather than trying to force prohibited credit card acceptance. PIN debit is the strongest fit for a physical checkout because it routes the transaction through an allowed bank-to-bank path instead of prohibited credit card rails.

The safest payment method depends on the channel. Don't use one rule for the counter, curbside, and delivery.

Train staff on scenarios, not slogans

Most dispensaries do some version of annual policy review. That's not enough. Staff remember stories better than rulebooks.

Use short drills:

- Terminal tampering drill: Show staff two payment devices and ask which one looks wrong.

- Refund manipulation drill: Walk through a fake void request and ask who should approve it.

- Delivery dispute drill: Review what proof must exist before a “not received” claim is accepted.

- Phishing drill for managers: Practice what to do when a vendor email asks for urgent credential changes.

Training should answer one question for each role. “What do I do in the moment?” If the answer is vague, the procedure isn't ready.

Secure delivery and pickup as separate workflows

A delivery order isn't just an in-store order with wheels. It needs its own controls.

A practical checklist:

| Workflow point | What to control |

|---|---|

| Order placement | Limit who can edit payment-related fields after submission |

| Checkout page | Inventory all scripts and plugins that load during payment |

| Handoff to delivery | Record who released the order and when |

| Arrival and proof | Require consistent proof-of-delivery steps |

| Disputes | Keep payment record, order timeline, and delivery confirmation together |

If you offer pickup or delivery through digital ordering, review the customer-facing flow the same way a stranger would. The process should feel simple to the buyer and tightly controlled behind the scenes. That same mindset also improves customer convenience in guides about how to order weed online, but the security side has to be designed deliberately.

How to Evaluate Payment Processing Vendors

A delivery order fails at checkout on a Friday night. Your staff sees a spinning payment screen. The delivery platform says the processor is up. The processor says the issue is in the embedded checkout. Your menu provider says it only passes the order through. Meanwhile, the patient is waiting, the driver is delayed, and no one can tell you who owns the problem.

That is the risk ownership gap. In omnichannel cannabis payments, the danger is not only fraud or PCI scope. The danger is a stack of vendors where each one controls part of the payment flow and no one takes full responsibility when something breaks or gets abused.

Ask who owns each layer of risk

Start with one plain question: who owns the payment experience at each step of the order?

For a dispensary, that usually means more than one environment. A customer may browse on one platform, pay through another component, get routed into your POS, then move into a delivery workflow with separate status updates and handoff records. That chain works like a relay race. If one runner drops the baton, the customer still blames your store.

“PCI compliant” is not a complete answer. It does not tell you who reviews payment page scripts, who approves changes, who watches for unauthorized code, or who leads the response if a checkout page is altered through a connected vendor. As noted earlier, payment page script accountability has become a major concern, especially where third-party ordering and delivery tools sit between the customer and the processor.

Ask these questions in writing:

- Who controls the payment page code and embedded checkout components?

- Who can add, remove, or update scripts?

- How are script changes reviewed and approved?

- Who monitors for unauthorized changes or injected code?

- Who contacts your team if suspicious behavior appears in the checkout flow?

- Who owns incident response if the problem starts in a delivery or curbside ordering tool?

If a vendor gives you vague answers, you still own the exposure.

Force clear answers before you sign

A vendor review should feel like hiring a security-sensitive contractor for your store. You would not hand over the keys because the sales pitch sounded polished. Payment access deserves the same discipline.

Use a practical screen:

- Cannabis workflow fit: Ask whether they support in-store, curbside, and delivery with different controls for each one.

- System map: Request a plain-language diagram showing what they host, what you host, and what outside providers host.

- Contract language: Review who is responsible if a breach begins in a plugin, script, API connection, or embedded payment element.

- After-hours response: Ask who answers during nights and weekends when a payment issue affects live orders.

- Data exposure: Confirm how they reduce your handling of sensitive payment data through encryption and tokenization.

- Operational impact: Check whether the controls are realistic for budtenders, managers, and delivery staff to follow under pressure.

One more test helps. Ask the vendor to walk through a fake incident: a suspicious script appears on the online checkout used for delivery orders. See how quickly they can tell you what happened, who investigates, what evidence they preserve, and what your team must do first.

Use red flags, not marketing language

Some vendor claims sound reassuring because they are broad enough to avoid accountability.

| Vendor statement | What it may really mean |

|---|---|

| “We handle compliance for you” | They may reduce part of your scope, but your business still carries merchant responsibility |

| “Our platform is secure by design” | Ask for the actual controls around scripts, permissions, change approval, and logging |

| “We integrate easily with delivery” | More integrations can create more places for orders or payment data to be exposed |

| “Support is available” | Confirm who responds during a live payment outage or suspected compromise |

Good payment design should also fit the buying experience your store wants to create. If checkout controls confuse patients or slow staff at the wrong moment, people invent workarounds, and workarounds create security gaps. That is why strong operators review vendor choices alongside the full dispensary customer experience, especially for curbside and delivery where trust can break down fast.

A strong vendor helps you answer three questions fast. What system failed? Who owns it? What is the next action? If those answers are blurry, you do not have a true payment partner. You have shared risk with unclear boundaries.

Navigating Specific DC Area Compliance Rules

Dispensaries in Washington, DC need to think locally even when the payment tools are national. The security controls may look familiar across markets, but compliance reality changes once you factor in DC medical cannabis rules, nearby delivery expectations, and the practical limits on payment types.

What matters most in the DC area

The first local issue is payment method fit. Because standard credit card acceptance is off the table for cannabis merchants, DC dispensaries have to build operations around compliant alternatives such as debit, ACH where appropriate, and cash. That means your compliance posture is tied not only to cybersecurity, but also to how well your daily procedures match the payment methods you employ.

The second issue is record consistency across channels. In-store, curbside, and delivery orders should produce a clean trail showing order creation, payment status, release, and completion. In DC-area operations, that matters because service often extends beyond a simple walk-in sale. The farther an order moves from the counter, the more important it is to preserve one reliable operational record.

The practical DC-area lens

For an owner serving patients in DC and nearby communities, the useful compliance questions are operational:

- Can staff explain why one payment option is allowed and another isn't?

- Can the business prove what happened during a disputed delivery order?

- Can management identify which vendor controlled the checkout environment for a given transaction?

- Can the team show that payment systems are separated from general business systems?

Those aren't abstract legal questions. They are the questions that surface when an auditor, banker, software provider, or internal manager tries to reconstruct an event.

Local compliance gets harder when a dispensary serves more than one buying pattern. Walk-in, curbside, and delivery each create different evidence trails.

For DC-area operators, the safest habit is to document the payment journey by channel. Treat in-store, curbside, and delivery as separate compliance paths with their own controls, approvals, and exception handling. That approach reduces confusion when a transaction is challenged and makes it easier to spot where a vendor, employee, or workflow is creating avoidable risk.

Your Next Steps for a Secure Dispensary

The strongest payment security programs don't rely on one tool or one policy. They rely on clear ownership. Someone owns the terminal checks. Someone owns the refund review. Someone owns the vendor relationship. Someone owns the delivery dispute process. If ownership is vague, risk spreads.

Start with three actions this week.

First, map your payment flow for each channel. In-store, curbside, and delivery should each have a simple diagram showing which system, person, and vendor touches the transaction.

Second, review every third-party checkout component. If a script runs on your payment page or order flow, identify it, document who approved it, and confirm who monitors it.

Third, test your evidence trail. Pick one recent order and see whether you can reconstruct the full story from payment to fulfillment without guessing.

Payment processing security isn't a one-time setup. It's an operating discipline. The dispensaries that stay stable are the ones that treat payments as a controlled process, not just a convenience feature.

If you're looking for a dispensary that takes compliance, payment clarity, and patient service seriously, Mr. Nice Guys DC is a trusted medical cannabis destination in Washington, DC. Patients can shop premium flower, edibles, vapes, concentrates, topicals, tinctures, and pre-rolls with convenient options for pickup, curbside, and delivery.

Mr Nice Guys DC

At Mr. Nice Guys DC, we’re more than just a cannabis delivery service — we’re passionate advocates for quality, convenience, and community. With years of experience in the cannabis industry, our team is dedicated to educating and empowering customers across Washington, D.C. Whether you're a seasoned user or just starting your cannabis journey, our blog delivers trusted tips, product insights, and the latest updates from the world of weed. Stay informed, stay elevated.